Indexation is looming – should you pay off a HECS debt before 1 June?

The Federal Government recently announced that the HECS-HELP annual indexation will increase to 7.1 per cent on 1 June this year, and according to BDO’s Marie Ryan it’s causing headaches for anyone wanting to enter the property market.

Photo: Brett Jordan

Only two years ago, indexation was a low 0.6 per cent, so most people didn’t give it a lot of thought, however it is now gaining some attention.

There is a small window in the next week-and-a-half to clear your HECS debt before the HECS indexation of 7.1 per cent is applied on 1 June 2023.

Home buyers who are saving for a deposit are asking whether they should pay down HECS to save on the indexation cost and questioning how that will impact their finance for their future purchase.

Since HECS impacts finance in multiple ways, the best way to proceed is very much a case-by-case basis.

Borrowing capacity

Banks include HECS as a commitment, generally calculated at the ATO threshold rate as a percentage of income – which is tiered and varies from nil for low-income earners (up to $48,360) to 10 per cent for those over $141,848.

For example, someone on $60,000 would have a commitment of $1,500pa (2.50 per cent of income) included in their loan servicing calculation.

Banks generally allow a maximum debt-to-income (DTI) ratio of six times. If HECS is included in the debt, it could take a borrower over the threshold.

Available deposit

HECS is generally highest for younger borrowers trying to get into the market and that’s the time when building a 20 per cent deposit is the main challenge for them. Clearing HECS debt is often simply not an option as it would deplete their hard-earned deposit and potentially put them into lenders mortgage insurance (LMI) territory, which erodes any savings from paying out HECS.

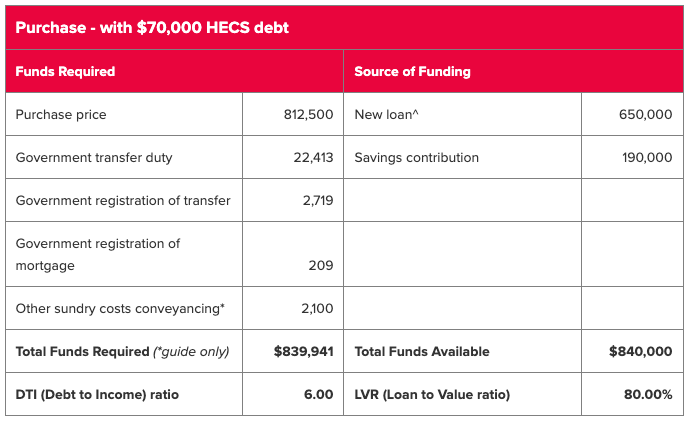

Case study

A couple wish to purchase a property to live in for $812,500. They have:

- Income of $120,000 ($60,000 each)

- HECS debt of $70,000 ($35,000 each)

- Available savings to contribute of $190,000

The total required for the purchase (including estimated purchase costs) is $840,000 and their maximum loan (including the HECS commitment) is $650,000, which means:

- Total available for the purchase is $840,000 (loan $650,000 + savings $190,000)

- They are able to buy the property for $812,500, covering 20 per cent deposit + costs so no LMI

In this scenario, although they incur HECS indexation of $4,970 @ 7.1 per cent of their $70,000 HECS debt, they have achieved their primary goal of purchasing their first home.

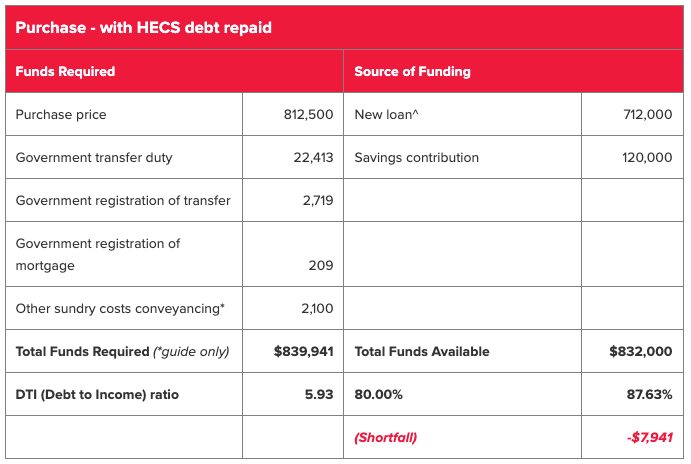

If they instead paid out their $70,000 HECS debt (to avoid the $4,970 indexation)

- Savings would reduce to $120,000

- Borrowing capacity would improve to $712,000 (without HECS commitment)

- Total available for the purchase would reduce to $832,000

For the same $812,500 purchase, they now have the situation of a $7,941 shortfall. As their deposit is now less than 20 per cent, an extra $12,000 LMI premium will be added to their home loan which would push them over their maximum borrowing capacity.

Although they have saved $4,970 indexation cost by paying out their HECS debt, their goal of buying the $812,500 home is no longer possible!

Paying out HECS is not necessarily the best strategy for this couple’s scenario.

A low-income earner with a 20 per cent deposit may be better off keeping the HECS debt intact, as they need their cash to avoid LMI and the impact on borrowing capacity is nominal.

However, paying out HECS could work well in some situations, such as couple with a larger deposit who may be better off clearing the HECS debt to improve borrowing capacity and avoid the 7.1 per cent indexation.

In summary, it is best to seek advice and do the sums before making the decision of whether paying out HECS is best for you.

For more information, please contact your local BDO Finance Solutions adviser.