Reviewing your superannuation now could pay big dividends in retirement

As the end of the financial year approaches it is time to review your superannuation to ensure you will have the best retirement possible.

New rules for super contributions. Photo: Getty

The best place to start is to look at the returns your fund is making in comparison to others along with the level of fees you are paying, and the amount of insurance your fund is providing you.

The difference between a top-performing super fund and an under-performer is the difference between a prosperous and a difficult retirement.

The following chart provided by Foreman Financial Group brings that into focus.

For a young person starting out in the workforce and living a working life on average earnings, a high-performing fund will deliver a $1.6 million retirement balance at age 70.

If you spend your working life in an under-performer then you will finish up with less than half of that.

The figures assume funds with moderate fees of 1.5 per cent annually and returns of 8.5, 6.5 and 4.5 per cent respectively, says Foreman director Tom Foreman.

“Even a 2 per cent difference over four years makes a massive difference,” Foreman said.

An average performance of 8.5 per cent over a working life is very hard to attain.

Chant West research shows that while the average growth fund, in which 90 per cent of Australians are invested, attained an 8.4 per cent return over three years, over 15 years the average return was 6.1 per cent.

But even if you are in a moderately performing fund you will still finish up with a retirement balance of $1 million plus.

And some of the big funds have performed better than the average over time.

“Hostplus has returned an average of 7.04 per cent over five years,” Foreman said.

What is the super target?

It’s good to know what you are aiming at as a retirement balance and check your progress along the way.

That way you can make adjustments to your savings plan as necessary and where possible.

The Association of Superannuation Funds of Australia (ASFA) targets what it calls a ‘comfortable retirement’ at $595,000 for a single homeowner and $690,000 for a couple.

So that should be possible to achieve for a young person spending a working life in a moderately performing fund.

While that progress may be possible for a young person starting work today and receiving the average wage with 12 per cent super from 2025, it isn’t the reality for many people today.

“Most people starting out now will hit those [ASFA] figures,” Foreman said. However, for older workers super has not delivered nearly as much as it will for future generations.

The super guarantee started at 2 per cent in 1992 and then moved to 9 per cent for a number of years.

“So if you’re 65 you will only have had super for 30 years and mostly at 9 per cent,” Foreman said.

The following table bears that reality out, with most Australians falling well short of achieving ASFA’s comfortable retirement standard.

But if you are not at the ASFA comfortable retirement level you can still have a reasonable retirement income by mixing the age pension with your superannuation assets.

If you are on a part pension you will draw more from the pension as your super assets decline.

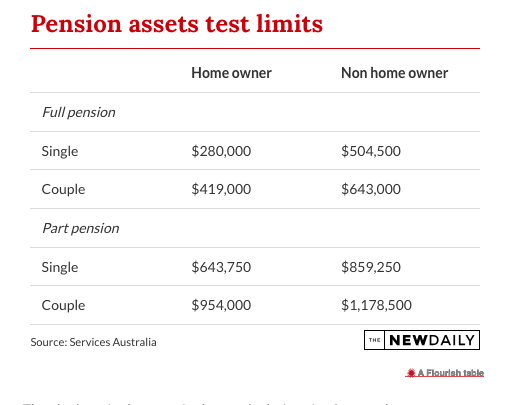

As the chart above shows, a home-owning couple can have up to $419,000 in super or other assets and still get a full pension – more if you don’t own a home.

For a part pension the same couple could have up to $954,000 in assets.

The elephant in the room in these calculations is of course home ownership, and that is declining for older people.

Of the current 60 to 64 years cohort, 78.3 per cent are homeowners compared to 80.5 per cent for those born immediately post-war, government figures show.

Making up some ground

If you are not where you would like to be in regards to retirement it’s not too late to make up a bit of ground.

Catch-up provisions mean you can make tax concessional super contributions back five years to 2018-19.

The measure allows you to make up the difference between the concessional super cap, now $27,500, and what your employer has paid you over the years.

“You can do it in one fell swoop if you like,” said Wayne Leggett, director of Paramount Financial Solutions.

However, if you aren’t cashed up you can still add more to your super through personal contributions, which has become easier.

“You don’t need to make salary sacrifice arrangements with your employer anymore. You just make the payments into super yourself,” Leggett said.

If you are doing that you can advise the Australian Taxation Office of your intention and they will adjust your fortnightly tax payments to take account of it rather than wait until the end of the year to claim back the tax deductions.

Check the returns your fund is making, and check that any insurance you are paying for through super meets your needs.

If you are in a position to make extra payments, do it now, Mr Leggett said.

“Time is your biggest ally, so start as soon as you think about it,” Leggett said.

This story first appeared in our sister publication The New Daily, which is owned by Industry Super Holdings