Superannuation fund pushes for ‘one account for life’

Combine accumulation and pension accounts into one before the avalanche of retirement hits the nation, says AustralianSuper.

There are a few different options when it comes to an income stream in retirement.

AustralianSuper has called for a series of superannuation reforms, including “one account for life” to deal with the massive rush towards retirement.

The nation’s largest super fund, with one in seven workers as members and a total of $316 billion under management, says 3 per cent of its membership is retired.

Their retirement balances account for 14 per cent of its asset base, or $46 billion.

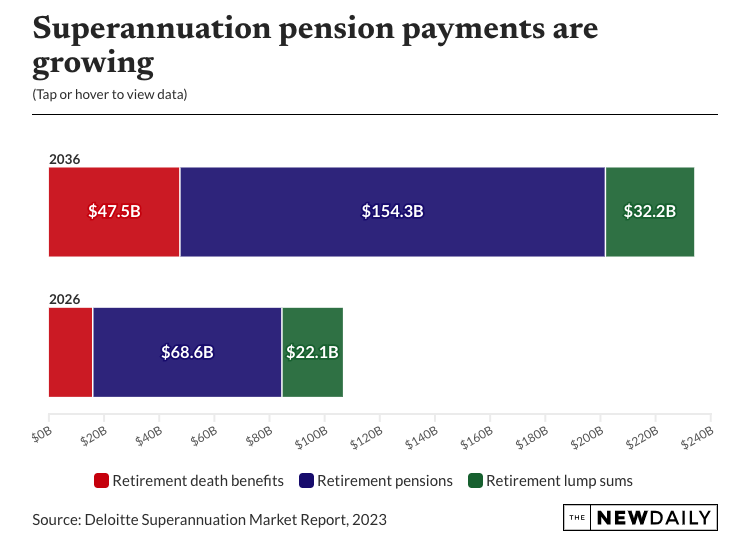

By 2030, the 65-plus population will hit 5.7 million and the vast majority of those will be fully or partly retired.

Currently, 1.6 million people are retired and receiving some benefit from superannuation.

Treasury has reported that drawdowns from superannuation will increase from 2.4 per cent of GDP in 2022-23 to 5.6 per cent of GDP in 2062-63.

In a recent submission to Treasury, AustralianSuper said this tidal wave of retirement demanded a different approach to retirement funding than currently in use.

Time for change

“We must radically shift our perspective from one that sees retirement as an end point for superannuation to one where it is viewed as a continuation,” the submission said.

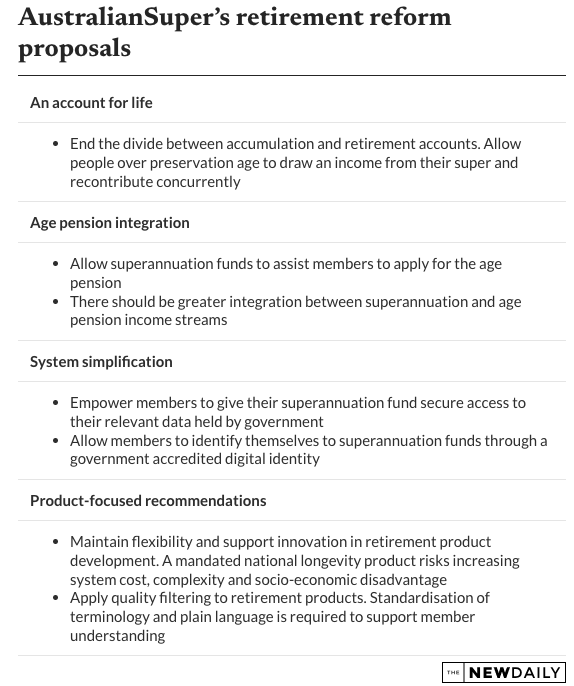

One way would be to introduce an “account for life” that would simplify members’ interactions with superannuation.

This would allow members to hold only one account from which they could draw pensions and make contributions.

The way the system currently works is that before retirement, members pay into a super accumulation account, and when they move into retirement they create an allocated pension which pays a tax-free income.

However, the border between work and retirement is increasingly fuzzy.

AustralianSuper reported that 8 per cent of its members plan never to fully retire and 20 per cent of those with super in pension mode are still in the workforce or planning to return to it.

“As the relationship between work and retirement evolves, many members are telling us they are struggling to navigate the complexities of a fragmented system, [with] the interplay of income from multiple income sources,” Shawn Blackmore, AustralianSuper’s chief retirement officer said.

Recent legislative changes have meant people can make contributions to super up to age 75.

Along with the government’s work bonus, which allows work income of up to $300 per fortnight to be earned without affecting age pension entitlements, this creates strong incentives for retirees to continue work.

They can choose to do this and draw down the statutory limit from their super balance in pension mode.

But doing that is complicated because it demands a retiree have two super accounts, one in pension mode and one in accumulation.

That means more paperwork and higher super fees because there are two accounts.

Simplicity is great

Rainmaker research director Alex Dunnin said the idea of a single superannuation account covering accumulation and retirement made sense.

“It would mean you don’t have to switch accounts, which involves filling in a lot of forms and deciding how much you want to withdraw from an account-based pension,” Dunnin said.

AustralianSuper’s report identified that the ageing of the population would push an increasingly wealthy cohort of people into retirement and with the growth of superannuation balances comes a more complex financial situation.

“The maturing of the system will bring profound changes for the nation. With the total population aged 65 and over forecast to grow from 4.1 million in 2020 to 5.7 million by 2030, the system needs an urgent focus on the ‘spending phase’,” the report found.

AustralianSuper’s own figures identify how superannuation is increasingly driving wealth of older Australians.

The average male 55-year-old member of the fund has $162,000 in super savings now, while for women the figure is $132,000, and those figures have increased 40 per cent in five years.

The fund’s submission to Treasury estimates that by 2043 the average account will have a balance of about $500,000, and those who start work now and enjoy super contributions of 12 per cent from 2025 will be in a far better position than that.

The whole proposal

AustralianSuper called for a number of other reforms beyond lifetime super accounts.

One measure growing in importance would be allowing super funds to help members apply for the age pension.

Currently, 32 per cent of retirees put off applying for the pension for a year or more after retirement.

As a result, they miss out on entitlements from the government and use up their super quicker than they otherwise might.

The submission recommends that super funds and the government share financial data to identify pension entitlements without waiting for the member to apply.

“Having a simple, seamless and, most importantly, integrated system in retirement, as they do in accumulation, will help retirees to navigate these changes with confidence,” Blackmore said.

This story first appeared in our sister publication The New Daily, which is owned by Industry Super Holdings.